EN

The Stock Exchange of Hong Kong Limited (the “Exchange”) and/or the Securities and Futures Commission (the “SFC”) recently published various guidance concerning, among other things, (1) the regulatory reform relating to the Uncertificated Securities Market (“USM”), which is expected to be implemented on 16 November 2026, and (2) the launch of a new issuer communication platform, the HKEX Issuer Access Platform (“IAP”), in the fourth quarter of 2026.

The Hong Kong USM regime aims to eliminate paper share certificates and facilitate the electronic holding and transfer of securities. At the core of the regime is the use of an Approved Securities Registrar (“ASR”), which will evidence and transfer securities through its Uncertificated Securities Registration and Transfer System, enabling investors to hold participating securities in uncertificated form directly in their own names and enjoy shareholder rights directly.

The key matters that listed issuers should note in relation to the USM regime are summarized below:

2.HKEX Issuer Access Platform (IAP)

The IAP is a new online communication platform established by the Exchange to unify regulatory filings, public submissions and two-way communications between listed issuers and the Exchange. A summary of the IAP is set out below.

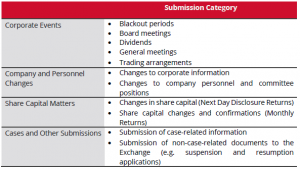

The IAP will consolidate a wide range of functions. In general, the documentary filings and categories of approvals that users may submit and process through the IAP include, but are not limited to, the followings:

The issuer’s authorised representatives, relevant employees, professional advisers, printers and other market participants authorised by the issuer may register accounts on the IAP and conduct the relevant filings and communications through the platform.

Upon launch, the IAP will operate alongside the Electronic Submission System (“ESS”) and will assume the electronic form submission functions currently handled through ESS. In general, the IAP will become the primary platform through which issuers and their advisers handle Listing Rules compliance matters while also facilitating the publication of the relevant announcements and circulars (such as those relating to notifiable transactions and/or connected transactions) through its integration with the ESS.

The Exchange currently plans to launch the IAP in the fourth quarter of 2026. The registration and onboarding process will be conducted in phases:

Following completion of the transition to the IAP, the Exchange will introduce a redesigned market information page on its website, consolidating and displaying issuer information such as management details, corporate events and other key dates. Once issuers update their records, investors will be able to access updated information on an almost real-time basis, further enhancing market transparency.

For further information or advice regarding (1) the USM regulatory reforms, and (2) the IAP, please do not hesitate to contact us.

Summary

In Li Yuhong v oOo Securities (HK) Group Ltd [2025] HKCFI 5270, the Hong Kong Court of First Instance found an investment adviser/asset manager liable for misrepresentation and multiple pre- and post-investment breaches of duty in connection with an investor’s subscription for unlisted corporate bonds.

The Court’s reasoning turned heavily on (i) the defendant’s conflicted “dual hat” role as both exclusive placing agent and discretionary asset manager, (ii) significant evidential gaps, and most notably, (iii) the defendant’s failure to call the relationship manager alleged to have made the key representations as a witness.

Key Facts

The plaintiff, a Mainland investor, sought Hong Kong residence under the Capital Investment Entrant Scheme (“CIES”). She initially invested in a comparatively lower-risk product. During the pre‑engagement period, the defendant’s relationship manager worked to build a relationship of trust with the family, and the defendant was appointed the exclusive placing agent of certain unlisted, non‑rated bonds issued by China Agroforestry Low‑Carbon Holding Company Limited (the “Issuer“) (the “Relevant Bonds”) in the value of HK$50 million, earning commission on placements .

The plaintiff was persuaded to switch her entire CIES investment into the Relevant Bonds through the defendant, acting as placing agent, for a total investment of HK$10.5 million. The parties also entered into a discretionary asset management agreement under which the defendant was to manage the bonds post-subscription, thereby earning additional management/performance fees.

The Issuer ultimately failed to redeem the bonds at maturity, and the plaintiff sustained an almost total loss.

Court’s findings

Adverse Inferences and Evidential Gaps

A decisive feature was the Court’s willingness to draw strong adverse inferences from missing witnesses and missing documents. The defendant did not call the former relationship manager alleged to have made the key representations as a witness; the Court described this omission as “critical if not fatal” and drew adverse inferences. The Court was also critical of the lack of contemporaneous internal records said to evidence portfolio monitoring and review.

Misrepresentation: “early redemption” and “low risk” assurances

The Court found that the defendant (through its relationship manager) made, and the plaintiff relied on, two central representations:

On the “early redemption” representation, the Court regarded the contemporaneous Client Analysis Report as pivotal: it contained a purported early redemption term which did not appear in the bond terms and conditions. The Court rejected the suggestion that this was a mere “clerical error”. The plaintiff’s later email correspondence in December 2018, referring to the same 30‑day notice understanding, was treated as consistent with that representation and was not corrected by the defendant’s staff at the time.

As to the “low risk / safe investment” representation, the Court held it was inherently more probable that a relationship manager seeking to complete a large primary‑market placement would “paint a rosy picture” to induce the investment, and noted the absence of documentary evidence that the defendant ever warned the plaintiff that the Issuer was loss‑making. The defendant’s only factual witness ultimately accepted he had no basis to deny the representation was made.

The Court also accepted the plaintiff’s expert evidence that the Relevant Bonds were high risk and unsuitable for the plaintiff’s pleaded investment objective, noting features such as the Issuer’s weak financial position, lack of independent credit rating, illiquidity, and concentration risk.

Contractual wording did not provide a safe harbour

The defendant relied on non-reliance/exemption wording in the placing documentation to argue that the misrepresentation claim was contractually precluded. The Court rejected this in substance, emphasising that fraudulent misrepresentation is not readily excluded absent clear wording, and that in any event such clauses are susceptible to statutory control.

Separately, the Court considered the plaintiff’s inability to understand the English-only placing letter, the rushed signing process, and the absence of explanation or translation, and accepted a non est factum analysis in the circumstances to negate the effect of the defendant’s attempted contractual protections.

Post-investment management: monitoring failures, exit options, and conflicts

Once the bonds were held within a discretionary management structure, the Court found that the defendant owed contractual, common law, statutory and/or fiduciary duties as asset manager/trustee, including duties of reasonable care and skill, monitoring, and fiduciary no-conflict/no-profit obligations.

On the facts, the Court found no evidence of meaningful monitoring and held that the defendant had either delayed or simply ignored the plaintiff’s redemption requests. The Court noted that the defendant’s staff had even sought clarification from the Issuer on the early redemption procedure, with no documentary evidence showing any considered decision‑making.

Crucially, the Court held that the defendant failed to exercise, or even properly consider, contractual exit rights that could have materially improved the plaintiff’s position as risks crystallised.

Finally, the Court held that the defendant’s dual roles, earning placing commission as exclusive placing agent while also charging management/performance fees as discretionary asset manager, engaged and breached fiduciary no-conflict and no-profit duties in the absence of fully informed consent.

Practical takeaways

This is a rare case where an investor succeeded in her claim against her investment adviser/asset manager for misrepresentation and breaches of duty.

Taken together, this judgment highlights several important lessons. Investment advisors must remain vigilant to conflicts of interest when acting in dual capacities, and should not assume that broad non‑reliance or exemption clauses will protect them as those clauses may be found unreasonable or unconscionable.

While outcomes in investor claims remain highly fact-sensitive, this decision illustrates that courts will hold advisers and discretionary managers to exacting standards where the evidential record does not support the intermediary’s account of advice, monitoring and conflict management.

MinterEllison has extensive experience assisting investors with asset recovery and helping corporations manage and resolve complex disputes involving financial products, advisory relationships, and asset management arrangements. For further information, please contact our Dispute Resolution team.

The full judgement can be accessed here: legalref.judiciary.hk/lrs/common/ju/ju_frame.jsp?DIS=175819&currpage=T

From January to April 2026, The Stock Exchange of Hong Kong Limited (the “Exchange”) published certain guidance covering, among other matters: (1) the uncertificated securities market (the “USM”); (2) revisions to the ongoing public float requirements; and (3) the appointment, removal and remuneration of auditors. This article summarises the key aspects of the relevant updates.

(1) Uncertificated Securities Market

The USM regime aims to abolish paper share certificates and enable the electronic holding and transfer of securities. The core feature of the USM is that, through the platforms operated by approved securities registrars (“ASR“) and connected to systems of Hong Kong Securities Clearing Company Limited, investors may hold prescribed securities (“Prescribed Securities“) directly in their own names in uncertificated form and enjoy shareholders’ rights directly. The Exchange and the Securities and Futures Commission currently expect the USM to be implemented on 16 November 2026 (“USM Implementation Date“), with the corresponding amendments to the Listing Rules taking effect upon the implementation of the relevant subsidiary legislations. The USM regime prescribes a five‑year phased mandatory transition, with an aim to enhance the operational efficiency and security of the securities market.

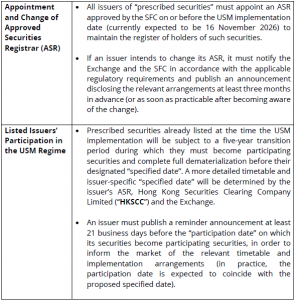

For new applicants of Prescribed Securities whose listing date falls after the USM Implementation Date, such securities must be issued in uncertificated form from the date of listing. Prescribed Securities of listed issuers will be required to become Participating Securities within the five‑year transition period from the USM Implementation Date. For listed issuers, there are certain preparatory steps which need to be completed at this stage, including (but not limited to):

|

Action required |

Relevant deadline |

|

| 1 | Appoint an ASR (no action required if the existing share registrar is already an ASR) | By USM Implementation Date (expected to be 16 November 2026) |

| 2 | Amend their constitutional documents (and/or terms of issue of the relevant securities) to align with applicable USM legal and regulatory requirements | Within one year from the USM Implementation Date |

| 3 | Ensure that the issuer’s constitutional documents allow the convening of general meetings where: (a) shareholders may attend meetings virtually using technology; and (b) shareholders may vote by electronic means. | Upon the constitution documents being updated (if required) |

| 4 | Announce the latest date by which their Prescribed Securities will become Participating Securities (referred to as “Specified Date”) | As soon as reasonably practicable and no later than one business day after being notified, by the Exchange, of their Specified Date |

| 5 | Establish arrangements to provide holders of securities with the option to send meeting and non‑meeting instructions electronically | From the USM Implementation Date, subject to a one‑year transition period for compliance with new Listing Rule 2.07D |

| 6 | Establish arrangements to provide holders of securities with the option to receive corporate action proceeds (e.g. dividends) electronically | From the USM Implementation Date, subject to a one‑year transition period for compliance with new Listing Rule 2.07E |

| 7 | Establish arrangements to provide holders of securities with the option to pay subscription monies electronically in connection with offers of new securities (e.g. rights issues or open offers) | From the USM Implementation Date, subject to a one‑year transition period for compliance with new Listing Rule 2.07F |

Listed issuers are therefore recommended to engage with their ASRs and assess whether preparatory work (such as amendments to constitutional documents) should be commenced in advance, in order to facilitate a smooth transition to the USM regime.

(2) Revisions to the Ongoing Public Float Requirements

The Exchange has revised the ongoing public float requirements under the Listing Rules. The revised rules have taken effect since 1 January 2026, introducing new ongoing public float thresholds, disclosure obligations and the regulatory approach to public float shortfalls.

While the existing minimum 25% public float requirement applicable to issuers (which have no other classes of listed shares) (the “Initial Prescribed Threshold“) will remain effective, the revised regime introduces an alternative threshold for compliance purpose. Under the alternative threshold, an issuer must ensure that the portion of the class of shares an issuer has listed on the Exchange that is held by the public must, at all times:

An issuer which intends to adopt the Alternative Threshold is required to publish an announcement as soon as practicable, containing the reasons for the change and a statement setting out the market value and percentage of its public float as at the latest practicable date.

For A+H share issuers, the revised rules replace the former aggregate threshold for both A and H shares with bespoke ongoing public float requirements for H shares. Under the new regime, at all times, the issuer’s H shares listed on the Exchange and held by the public must either:

In addition to the longstanding requirement to confirm sufficient public float in annual reports, the revised regime introduces ongoing disclosure requirements at both monthly return and annual report levels, summarised below:

|

Reporting obligation |

Monthly returns |

Annual report |

| Confirmation of compliance with the applicable ongoing public float threshold | All issuers | All issuers |

| Minimum public float percentage threshold | Issuers relying on the Initial Prescribed Threshold | Issuers relying on the Initial Prescribed Threshold |

| Actual public float percentage | Issuers relying on the Market Value Thresholds | All issuers |

| Actual public float marker value | Issuers relying on the Market Value Thresholds | Issuers relying on the Market Value Thresholds |

| Share ownership composition | Not applicable | All issuers |

| Share capital structure | Not applicable | All issuers |

The revised regime also removes automatic suspension solely due to a public float shortfall and adopts a disclosure‑ and remedial‑based approach.

For all issuers with a public float shortfall:

For issuers with a Significant Public Float Shortfall (as defined under Rule 13.32F of the Listing Rules), additional requirements apply, including:

(3) Latest FAQs on the Appointment, Removal and Remuneration of Auditors

The Exchange has also updated FAQ16 – No.5 to provide further clarification on the core shareholder protection standards relating to the appointment, removal and remuneration of auditors under paragraph 17 of Appendix A1 to the Listing Rules.

Under the relevant guidance, a listed issuer must ensure that the appointment, removal and remuneration of its auditors are approved by a majority of shareholders, or by another body that is independent of the board of directors. The Exchange has confirmed that, where a listed issuer’s constitutional documents:

such arrangements will generally be regarded as meeting the core shareholder protection standards, provided they are consistent with the applicable provisions of the Companies Ordinance (Cap. 622) (or the equivalent provisions in the issuer’s constitutional documents and domestic laws).

In addition, to ensure that the appointment or re‑appointment of auditors is considered through due process, the Exchange has indicated that the relevant circular should disclose the estimated audit fee agreed with the auditor for the audit services for the relevant reporting period (whether as a fixed amount or a fee range), together with an explanation of the basis of determination and key assumptions adopted.

Importantly, the Exchange has emphasised that a listed issuer must not request or take any action to cause an auditor to resign without first obtaining shareholders’ approval at a general meeting, as such request or action may be regarded as a removal of the auditor under the Listing Rules. The Exchange has further cautioned that pressuring an existing auditor to materially reduce previously agreed audit fees, whether directly or by reference to lower quotes from other auditors, may be regarded as indirectly causing an auditor’s resignation in lieu of shareholders’ approval.

For further information or advice regarding the above, please do not hesitate to contact us.

In HCA 215/2025, the Hong Kong Court of First Instance considered an application by the Securities and Futures Commission (SFC) for interlocutory injunctive relief under both the Court’s Mareva jurisdiction and section 213 of the Securities and Futures Ordinance (SFO).

The civil proceedings arose out of alleged market manipulation involving the shares of KNT Holdings Limited (KNT), a company listed on the Main Board of The Stock Exchange of Hong Kong. The SFC alleged that a group of defendants had perpetrated a “ramp-and-dump” scheme in 2019, artificially inflating KNT’s share price before disposing of their holdings at substantial profit, causing significant losses to market investors. At the time of the civil application, criminal proceedings under section 300 of the SFO had already been commenced against a number of defendants and were ongoing.

The application

The SFC sought interlocutory injunctions restraining several defendants from disposing of, dealing with or diminishing the value of their assets in Hong Kong, up to approximately HK$219 million, with the stated purpose of preserving assets for potential compensation and restoration orders if contraventions were ultimately established.

The application was resisted on multiple grounds, including alleged delay, the existence of parallel criminal proceedings, the presence of other enforcement measures, and submissions that the civil action was unnecessary or duplicative.

Key findings

The Court granted the injunctions.

First, it held that the SFC had shown a good arguable case of contravention of section 300 of the SFO, and that there was a real risk of dissipation of assets absent injunctive relief. The Court was satisfied that the evidence, including expert analysis of trading data, supported the allegation of a coordinated scheme and justified interim protection.

Secondly, the Court rejected the argument that the civil proceedings merely duplicated the criminal process. In doing so, the Court made clear that section 213 proceedings serve a distinct function, stating:

“I am unable to agree that the present action only serves as an insurance for the criminal proceedings. This Action has its own utility and function and there is no issue of duplicity. The interlocutory injunctions sought are to ensure that any compensatory and restoration orders granted in the Action would not be rendered nugatory.”

The existence of parallel criminal prosecutions did not therefore deprive the civil action of utility or render it oppressive.

Thirdly, the Court held that delay, in itself, was not a bar to relief. The relevant question remained whether there was a real risk of dissipation. In light of the complexity of the alleged scheme and the volume of material investigated, the Court accepted the explanation for the time taken and found no culpable delay.

The Court also rejected submissions that existing enforcement measures were sufficient. Those measures served different purposes, applied different thresholds, and did not cover assets that had not been fully disclosed. In that context, section 213 injunctions remained necessary.

Finally, the Court reaffirmed that the SFC, acting as a public authority enforcing statutory duties in the public interest, was not required to give a cross‑undertaking in damages when seeking injunctive relief under section 213 of the SFO.

Takeaways

The decision illustrates how courts approach applications for early civil asset‑preservation relief under section 213, including where criminal proceedings are already underway. It confirms that civil enforcement under section 213 is not ancillary to prosecution, but operates as a distinct statutory mechanism subject to judicial scrutiny and public‑law principles.

For companies and individuals under investigation, the case underscores that regulatory exposure may crystallise across multiple forums at the same time, and that investigative and interim stages may carry immediate and legally enforceable consequences.

The full judgment can be accessed here.

On 11 February 2026, the Insurance Authority (the “IA“) published the consultation paper on proposed amendments to the Insurance (Valuation and Capital) Rules (Cap. 41R) (the “Consultation Paper“). These proposals were made following the IA’s review of the current Risk-based Capital Regime (the “RBC Regime“), which was first introduced in July 2024 to replace the previous solvency margin approach with a modular approach for an assessment more sensitive to each insurer’s risk profile.

The proposed amendments are intended to promote infrastructure financing and strengthen Hong Kong’s role as a global risk‑management hub, while maintaining prudent safeguards.

They cover three areas, namely:

The full Consultation Paper is available at the IA’s website. The deadline for submitting feedback is 10 March 2026.

See news from our global offices